The Pulse of a Nation: A History of the Indian Stock Market and Its Evolution

The story of the Indian stock market is not merely a tale of numbers, charts, and trading volumes. It is a vibrant, dynamic narrative that mirrors the nation’s own journey from a colonial agrarian economy to a global economic powerhouse. It’s a saga of resilience, reinvention, and an unwavering belief in the potential of India’s capital. This history is intertwined with the ambitions of visionary entrepreneurs, the growth of the middle class, the evolution of financial regulation, and the relentless march of technological innovation. From a handful of brokers under a banyan tree to high-frequency algorithms and global integration, the Indian stock market has navigated through bubbles, scams, wars, and reforms, emerging stronger and more sophisticated with each passing era. Understanding this history is crucial not just for investors and financial professionals, but for anyone seeking to grasp the economic and social transformation of modern India.

Understanding the History of Indian Stock Market is crucial not just for investors and financial professionals, but for anyone seeking to grasp the economic and social transformation of modern India.

The Roots (1875 – 1947): The Banyan Tree to The Exchange

Understanding the History of Indian Stock Market

While informal trading of company shares and government bonds existed even earlier, the formal foundations of the Indian stock market were laid during the 19th century, primarily driven by the growth of British mercantile activity and the need to finance the development of railways and infrastructure.

The Cotton Mania and the First Crash

The catalyst for the creation of a formal stock exchange was, ironically, a market crash. The 1860s witnessed a cotton boom in Bombay (now Mumbai) as the American Civil War disrupted supply chains, sending cotton prices soaring. This led to a speculative frenzy, with numerous joint-stock companies being floated, often with dubious backing. However, when the Civil War ended and cotton prices collapsed, the bubble burst, causing widespread financial ruin. This event highlighted the urgent need for a regulated marketplace.

The Birth under the Banyan Tree: 1875

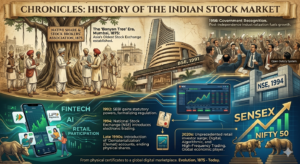

In 1875, a group of stockbrokers, who previously met under a large banyan tree in Mumbai (near where the Phiroze Jeejeebhoy Towers now stand), decided to organize themselves. They formed the “Native Share & Stock Brokers’ Association.” This association became the predecessor to the Bombay Stock Exchange (BSE), making it Asia’s oldest stock exchange. Initially, trading was entirely physical. Brokers would gather, yell orders (the “open outcry system”), and exchange physical share certificates. The primary shares traded were related to cotton mills, jute companies, and coal mines, reflecting the dominant industries of the colonial economy.

The Early 20th Century: War, Depressions, and Growing Domestic Capital

The early 20th century saw the gradual maturation of the market. The BSE introduced a ‘governing body’ and rules for trading, though they remained relatively rudimentary. The market was highly sensitive to global events, such as the two World Wars and the Great Depression. During World War I, increased industrial activity related to the war effort boosted corporate profits and stock prices, though volatility was high.

This period also saw the gradual rise of domestic Indian capital. Families like the Tatas and Birlas began to expand their industrial empires, leading to more large, domestically owned companies being listed. For instance, the founding of Tata Steel (TISCO) in 1907 was a milestone, marking the entry of heavy industry into the Indian corporate landscape and its subsequent presence on the exchange. However, the market remained predominantly institutional and focused on a limited number of “blue-chip” companies. The general public’s participation was minimal.

The Post-Independence Transition (1947 – 1991): The Licensing Era and State-Led Growth

The dawn of independence in 1947 marked a dramatic shift in India’s economic philosophy. The new government, led by Prime Minister Jawaharlal Nehru, adopted a socialist model with a focus on centralized planning and a dominant public sector. This period had a profound effect on the nature and growth of the stock market.

Centralized Planning and the Licence Raj

Under the “Licence Raj,” the government tightly controlled the economy. Companies required licenses for everything—from expansion and production quotas to pricing and capital raising. This stifled private enterprise and innovation. The growth of the stock market slowed considerably. Government-owned entities (Public Sector Undertakings or PSUs) and financial institutions became the dominant economic actors. The government utilized state-owned banks and insurance companies to mobilize savings and direct them toward government-mandated priorities, often away from the private capital market.

Major Institutions and Nationalization

The 1950s and 60s were characterized by the establishment of major financial institutions and the nationalization of key sectors.

-

1956: The Government of India formally recognized the BSE as the premier stock exchange.

-

1969: A pivotal moment occurred with the nationalization of 14 major commercial banks. This centralized control over credit and further limited the role of the market in capital allocation.

-

Nationalization of Insurance: Similarly, the creation of the Life Insurance Corporation of India (LIC) in 1956 and the General Insurance Corporation of India (GIC) in 1972 further consolidated the government’s grip on domestic savings. These institutions became massive, state-directed investors, often providing “backstop” support to the market rather than acting as profit-oriented, efficiency-seeking participants.

The Enduring Spirit of Equity Culture: The Rise of Dhirubhai Ambani

Despite the challenging regulatory environment, the desire for equity participation persisted. The late 1970s witnessed a cultural shift driven significantly by a single individual: Dhirubhai Ambani, the founder of Reliance Industries.

In 1977, Reliance Industries went public. Unlike his predecessors, who relied on large banks or a small circle of rich investors, Ambani made a strategic decision to appeal directly to the growing Indian middle class. He traveled across the country, convincing ordinary Indians to invest in his vision. The spectacular performance of Reliance shares, and the regular issuance of rights and bonus shares, transformed hundreds of thousands of small investors into wealthy individuals. Ambani effectively “democratized” equity investment in India, laying the foundation for a broad-based equity culture and sparking a renewed interest in the stock market. His strategy demonstrated that a strong domestic retail investor base could be a powerful force in the market.

The 1980s: Growth, and the First Crises of the Modern Era

The success of Reliance, along with the gradual liberalization steps taken by the government of Rajiv Gandhi in the 1980s, led to a surge in market activity. More companies were listed, trading volumes increased, and stock indices began to climb. The BSE SENSEX, the exchange’s main index, was introduced in 1986, creating a standard benchmark.

However, this rapid growth was not without its pitfalls. The unregulated and opaque nature of the market made it susceptible to manipulation. This era was punctuated by the market scams of the early 1990s, the most prominent being the 1992 Security Scam, led by Harshad Mehta. Mehta exploited loopholes in the bank receipt system to channel vast amounts of capital from banks into the stock market, creating an artificial bull run. The subsequent collapse wiped out hundreds of thousands of investors and severely damaged public confidence.

Liberalization and Transformation (1991 – 2008): The Birth of Modern Infrastructure

The 1992 scam was a watershed moment, but its impact cannot be separated from the broader economic transformation underway. In 1991, India faced a severe balance of payments crisis. In response, Finance Minister Manmohan Singh, with the full backing of Prime Minister P.V. Narasimha Rao, launched a historic process of economic liberalization. The market-led reforms—known as LPG (Liberalization, Privatization, and Globalization)—were essential to rejuvenate the economy, but they also highlighted the critical deficiencies of India’s capital market infrastructure.

SEBI and Statutory Powers: The Regulator Takes Control

Prior to 1992, the market was largely self-regulated, with oversight by the government’s Controller of Capital Issues (CCI), which had limited powers. The 1992 scam exposed the inadequacy of this system. In response, the government transformed the Securities and Exchange Board of India (SEBI) into a statutory body, giving it comprehensive regulatory powers to oversee the entire securities market. SEBI’s mandate was simple but profound: to protect investors, promote market development, and regulate the securities market. SEBI introduced a raft of regulations—from the introduction of automated trading systems and strict disclosure norms to regulations for mutual funds, foreign portfolio investors, and mergers and acquisitions. It began to lay down the code of conduct that governs the market today.

The Technological Revolution: Electronic Trading and Dematerialization

Perhaps the most significant transformation during this period was technological. The physical trading and settlement system was slow, inefficient, and prone to bad deliveries and theft. This had to change.

-

1994: The Launch of the National Stock Exchange (NSE): The NSE was established as a high-tech alternative to the BSE. It introduced an efficient, anonymous, order-driven, fully automated screen-based trading system. For the first time, brokers across India could trade on a single, integrated platform with real-time price dissemination. This innovation brought unprecedented transparency and accessibility to the market.

-

1995: The BSE Converts to BOLT: Faced with competition from the NSE, the BSE was forced to automate. It introduced its own screen-based trading system, BOLT (BSE Online Trading), effectively ending the traditional ‘open outcry’ era.

-

The NSE’s NIFTY 50: The NSE also introduced its flagship index, the NIFTY 50, in 1996, which rapidly established itself as a globally recognized benchmark for the Indian market.

-

The Dematerialization Revolution: Along with electronic trading came the need for digital settlement. The introduction of dematerialization (or ‘demat’ accounts) in the late 1990s was a monumental achievement. This process converted physical share certificates into electronic records, drastically reducing the time, cost, and risks associated with share settlement and transfer.

These technological changes democratized access, allowing anyone, anywhere in India, to trade easily. They also boosted liquidity, improved price discovery, and enhanced the overall integrity of the market.

Globalization and the Surge of Foreign Capital

As India’s economy liberalized, it began to attract the attention of global investors. The government gradually relaxed restrictions on foreign portfolio investment.

-

1992: FIIs (Foreign Institutional Investors) were allowed to invest in Indian capital markets, subject to specific limits. This brought massive amounts of capital, global best practices, and international research to India. FII inflows became a major driver of the Indian market, often determining its direction.

-

Emerging Global Recognition: India, along with countries like Brazil, Russia, China, and later South Africa (the BRICS), became a core component of “emerging market” portfolios. Large global companies and sovereign wealth funds started to allocate significant percentages of their capital to India, drawn by its demographic dividend, growing middle class, and strong economic growth. The early 2000s witnessed a sustained bull run, largely fueled by FII investments. The SENSEX, which was around 3,000 in early 2002, soared to over 20,000 by January 2008.

The Birth of Modern Asset Management

The transformation was not limited to the exchanges. The asset management industry also evolved. The entry of foreign and private domestic players into the mutual fund market brought competition and innovation. The establishment of companies like HDFC Asset Management and the entry of global giants meant that Indian investors had access to a wide variety of professionally managed products. This period also saw the introduction of the first Exchange Traded Funds (ETFs) and the growth of private equity and venture capital, diversifying the ecosystem of institutional capital.

Scams, Crashes, and Rebuilding (2008 – Present): The Digital Edge and Resilient Markets

The phenomenal bull run of the early 2000s came to a grinding halt with the onset of the Global Financial Crisis in 2008. The crisis demonstrated that the Indian market, while much more resilient than in the past, was not immune to global systemic risks.

The 2008 Crash: A Test of Resilience

The collapse of Lehman Brothers and the subsequent global credit freeze led to a panic among foreign investors, who pulled vast amounts of capital from emerging markets, including India. The Indian stock market suffered a massive collapse. The SENSEX lost nearly 50% of its value within a year, plummeting from over 20,000 to below 10,000 by early 2009.

However, the post-2008 period also revealed the underlying strength and resilience of the Indian market. Several factors contributed to a relatively swift recovery:

-

Strong Economic Fundamentals: India’s underlying economic story remained robust.

-

Swift Government Response: The government and the RBI launched aggressive fiscal and monetary stimulus to support the economy.

-

The Rise of Domestic Retail and Institutional Investors: Crucially, while FIIs were pulling out, domestic institutional investors (DIIs), led by LIC and the emerging mutual fund industry, stepped in to absorb the selling pressure. This development was pivotal, indicating that the market was no longer solely dependent on foreign capital. The increasing participation of domestic mutual funds, fueled by Systematic Investment Plans (SIPs), provided a crucial source of steady, long-term capital.

The Tech 2.0 Revolution and FinTech

The recovery was also propelled by a new wave of technological innovation. The period from 2010 to the present has been marked by a profound digital revolution.

-

Data Boom: The widespread availability of affordable 4G data, particularly through providers like Reliance Jio, led to an explosion in internet and smartphone penetration. This, in turn, fueled the growth of e-commerce, digital payments, and fintech.

-

India Stack: The “India Stack,” comprising Aadhaar (a unique digital identity), the United Payments Interface (UPI) (for instant, real-time payments), and other digital public goods, created a robust digital infrastructure. This infrastructure became the bedrock for a new ecosystem of online financial services.

-

Fintech Disruptors: Traditional brokerages were challenged by a new generation of discount brokers and fintech apps. Companies like Zerodha, Upstox, and Groww introduced commission-free or low-cost trading, intuitive user interfaces, and direct mutual fund platforms. They targeted a younger, tech-savvy generation of retail investors, leading to an unprecedented surge in new Demat account openings. The number of Demat accounts in India grew from around 20 million in 2014 to over 100 million by 2022.

The Startup Ecosystem: From Venture to IPO

The 2010s also saw the rise of a vibrant startup ecosystem, supported by private equity and venture capital. While these companies initially relied on private funding, they eventually sought public listing. The 2021-2022 period witnessed a flurry of tech-enabled startups, from Paytm and Zomato to Nykaa and PolicyBazaar, going public. While these initial public offerings (IPOs) were met with immense retail enthusiasm, they also faced scrutiny due to their high valuations and lack of profitability, highlighting the new challenges and complexities of a maturing market.

Unprecedented Resilience: COVID-19 and Beyond

The resilience of the Indian stock market was tested yet again during the COVID-19 pandemic. When the first nationwide lockdown was announced in March 2020, the market crashed spectacularly, with the NIFTY 50 falling by nearly 40% in just one month. The widespread fear of economic collapse led to massive selling.

However, the recovery was even more breathtaking. Within 18 months, the NIFTY 50 and SENSEX had not only recovered all their losses but had also nearly doubled in value from the pandemic low, driven by a combination of global liquidity, a faster-than-expected economic rebound, and a massive, continuous influx of domestic retail capital. This remarkable V-shaped recovery cemented the perception of India as a highly resilient market and highlighted the critical role that a committed domestic investor base can play.

New Horizons: Derivative Growth, Algo Trading, and Market Hours

Today’s market continues to innovate and evolve.

-

Explosive Derivative Volume: The derivatives segment (Futures & Options) on both the NSE and BSE has seen massive growth, transforming the Indian derivatives market into one of the largest and most liquid globally. While this has provided avenues for sophisticated hedging and speculation, it has also raised concerns about systemic risk and the participation of retail investors in complex instruments.

-

Algo and HFT: Algorithmic and High-Frequency Trading (HFT) are now dominant forces, accounting for a large portion of daily trading volumes, driven by advanced technological infrastructure and colocation services.

-

Globalization of Indices and Trading Hours: The market is now closely integrated with the global financial system. Decisions by the US Federal Reserve, global geopolitical events, and commodity price changes instantly ripple through the Indian exchanges. Discussions are now underway about extending trading hours to better align with global markets, further underlining India’s integration.

A Legacy of Evolution, A Future of Promise

The history of the Indian stock market is a fascinating and complex saga. It has evolved from a simple club for physical share exchange into a sophisticated, regulated, digitally enabled global marketplace. It has been a reflection of India’s challenges, with its history punctuated by speculative bubbles, devastating scams, and deep crises. However, it has also been a story of incredible resilience, with each challenge serving as a catalyst for reform, innovation, and stronger market infrastructure.

The Indian stock market’s growth has played a pivotal role in India’s development. It has helped private enterprise to mobilize capital, provided a means for the middle class to grow their wealth, and integrated India into the global financial architecture. Today, the Indian market is one of the world’s major capital centers, with a vibrant ecosystem of institutions, regulations, and technologies.

Looking ahead, the future of the Indian stock market appears promising, but not without its share of challenges. The continued financialization of household savings, the increasing application of AI and machine learning, and the relentless growth of the fintech ecosystem are likely to drive the market to even greater heights. However, the market must also grapple with issues of cyber security, the need for enhanced retail investor education, and the continuous challenge of preventing new forms of market manipulation.

Ultimately, the pulse of the nation beats within its stock market. It is a story of human ambition, technological prowess, and a relentless pursuit of a better economic future. As India embarks on its journey toward a multi-trillion-dollar economy, its stock market will remain a critical partner, a mirror of its progress, and a testament to its enduring entrepreneurial spirit. The banyan tree in Mumbai may be long gone, but the roots it planted have grown into a vast and powerful ecosystem, driving the dreams and aspirations of an entire nation.

_______________________________________________________________________________________

Visit : www.dkbtech.com and www.allcircular.com